When even Ben Bernanke, the former chairman of the Federal Reserve, can’t get a loan to refinance his mortgage, you know conditions are tight. Bernanke was turned down in seeking to refinance his mortgage in 2014, and though the mortgage industry has eased up somewhat since then, for many, the prospect of owning a home or getting a refinance loan is still a distant one. A forthcoming report by the Federal Financial Institutions Examination Council (FFIEC) will reveal just how distant.

Lending seized up after the fallout from overly lax practices during the housing boom. After the bust, financial institutions tightened their practices, requiring more money down and higher credit scores. As a result, the number of new mortgages issued plummeted. As we reported previously, mortgage lending in 2014 in the Chicago region hit a low of 8.1 new mortgages for every 100 homes. In 2005, in contrast, the rate was more than 29 per 100 homes. (Although some of that lending in 2005 was overly lax, credit was nevertheless more widely available.)

The FFIEC’s release of 2014 data on mortgage lending will reveal whether Chicago was an outlier or a bellwether. The data span all transactions at U.S. financial institutions covered by the Home Mortgage Disclosure Act (HMDA), including applications, originations, purchases and sales of mortgage and refinance loans, denials, and other actions.

Last year’s HMDA report, which covered transactions in 2013, found some progress, though not for everyone. Blacks and Hispanics, for example, were turned down for home loans in 2013 at nearly three times the rate of white borrowers—29 percent and 22 percent versus 11 percent for whites. Similarly, home purchase loans made to black and Hispanic borrowers declined slightly between 2012 and 2013.

Loans to lower-income borrowers were down sharply as well. The share of home purchase loans to borrowers with income of less than 80 percent of area median income declined from nearly 31 percent in 2012 to about 26 percent in 2013, according to the HMDA report.

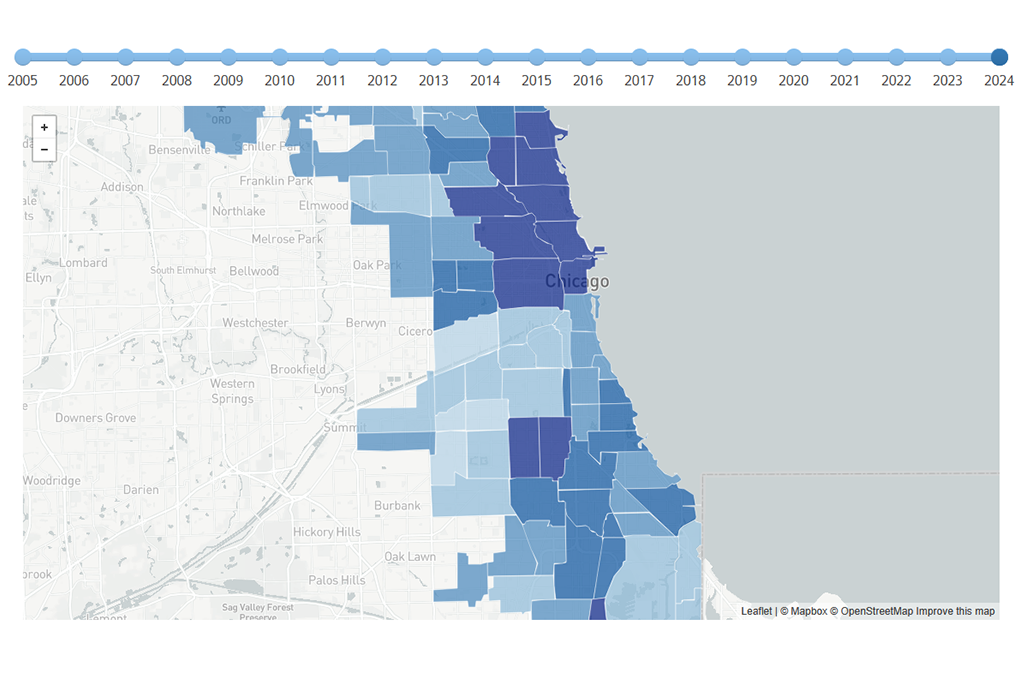

But that was 2013. The economy has picked up and signs look better for many families. However, one year later in 2014, our own data show that mortgage credit was still tight and neighborhood patterns of borrowing were clear, particularly in the West and South sides of the city and lower-income neighborhoods. Map 1 below shows patterns of mortgage lending per 100 residential parcels in 2014 for the Chicago region, while Map 2 zooms in to highlight 2014 lending patterns in the City of Chicago.

On the south and west sides, homes in the neighborhoods with the least activity are often older stock, lower value, in neighborhoods with high foreclosure rates and prices that have rebounded little since 2012. As our data show, in those neighborhoods, lending patterns were significantly below citywide averages. In areas such as South Lawndale, West Pullman, New City, South Chicago, and Roseland, for example, mortgage originations were only 3.5 or less per 100 homes, whereas the city average was 7.7. Likewise in Chatham, the rate of mortgage originations was 5.1, and in Auburn Gresham, it was 4.9. On the Northside, where housing trends are more stable, with fewer foreclosures or distressed housing, for example, mortgage lending was more robust. In North Center, for example, the rate of mortgage originations in 2014 was 16.3, and in Lakeview it 12.4.

Some have argued that the slow mortgage activity is not only due to a tight credit market.

“The reality is that this is as much a demand-driven drought as it is a credit-driven drought,” Joshua Rosner, of Graham Fisher & Company, a research firm, told the New York Times last October. An aging population, stagnant wages, and a wariness of taking on new debt have all reduced demand for mortgages, he and others argue. In addition, the housing crisis stripped many black and Hispanic families of home equity, their main asset, leaving them little to start over with. That said, for lower and middle-income renters, the heightened lending demands for both down payments and credit scores are likely an important factor in the sluggish lending patterns. The 2014 HMDA will reveal just how important.