It is generally assumed that the vast majority of residential property purchases are financed with a mortgage. While this is still often the case, one of the many ways in which the U.S. housing market has changed in the wake of the foreclosure crisis is that the share of residential properties purchased in cash is far greater than it was before the crisis began. This post provides an update on the growing role of cash buyers in Cook County’s housing market and the reasons buyers may purchase in cash. It includes a discussion of where buyers are making cash purchases of non-foreclosure-distressed properties in Cook County and concludes by taking a closer look at three Chicago census tracts that had higher levels of sales that were cash purchases of non-distressed properties in 2012.

Several recent stories have highlighted the high percentage of residential properties purchased with cash both locally and nationally. In Cook County, nearly half of all residential properties sold in 2012 were purchased with cash; findings reflected in recent analysis of the U.S. housing market which found that more than half of all homes sold in the last year were bought without a mortgage. This is a drastic change from the role that cash buying played in the housing market pre-crisis. In 2005, before the housing crisis began, cash purchases made up about 20 percent of all residential sales nationwide and around 15 percent of sales in Cook County.

IHS analysis of the characteristics of property purchases in our 2012 report Cash or Credit: The Role of Cash Buyers in Cook County’s Housing Market examined the increasingly important role cash buyers are playing in the wake of the housing crisis, particularly in certain neighborhood markets. It found that between 2005 and 2011 in Cook County, property sales financed with a mortgage declined 76 percent. While the number of cash sales increased by only 12 percent, the decline of financed purchases resulted in a market in 2011 where cash purchases made up 45 percent of total property sales.

Updated data for 2012, available on the IHS Housing Market Indicators Portal, show the share of homes purchased with cash in Cook County in 2012 increased to 46.5 percent. In the City of Chicago, cash buying increased from 47.9 percent of all residential property purchases in 2011 to 48.8 percent in 2012.

Why a buyer may choose to use cash

There are many reasons why a buyer may choose to pay for property using cash. In both strong and weak neighborhood housing markets, cash buyers may be investors buying homes to either rehab and quickly re-sell or rent for some amount of time. Cash buyers who intend to live in the property may prefer to use cash over financing because they have cash on hand from a sale of a previous home in which they had substantial equity, or they may simply have access to large amounts of cash based on their own personal assets. They can also be buyers who have trouble accessing credit but who have cash available to purchase a home.

Cash buyers often enjoy an advantage over buyers financing their purchase with a mortgage. Because cash transactions do not require mortgage underwriting, they can be completed more quickly than a financed transaction and do not bear the risk of the mortgage being denied. Because of this, sellers will often take a lower price for transactions completed with cash.

Analysis in the Cash or Credit report found that cash purchases are generally purchases of distressed properties, particularly in markets that have been heavily impacted by the foreclosure crisis. Foreclosure-distressed properties include properties purchased through short sale, at auction house, or out of REO/bank-owned inventory. Foreclosure-distressed properties are more likely to be purchased in cash than with a mortgage for a variety of reasons. Properties bought out of REO inventory, for instance, may be priced too low or in too poor a physical condition to qualify for a mortgage. (For more information on distressed properties and their role in cash buying, see the discussion beginning on page 12 of the full Cash or Credit report).

Where in Cook County properties are being purchased in cash

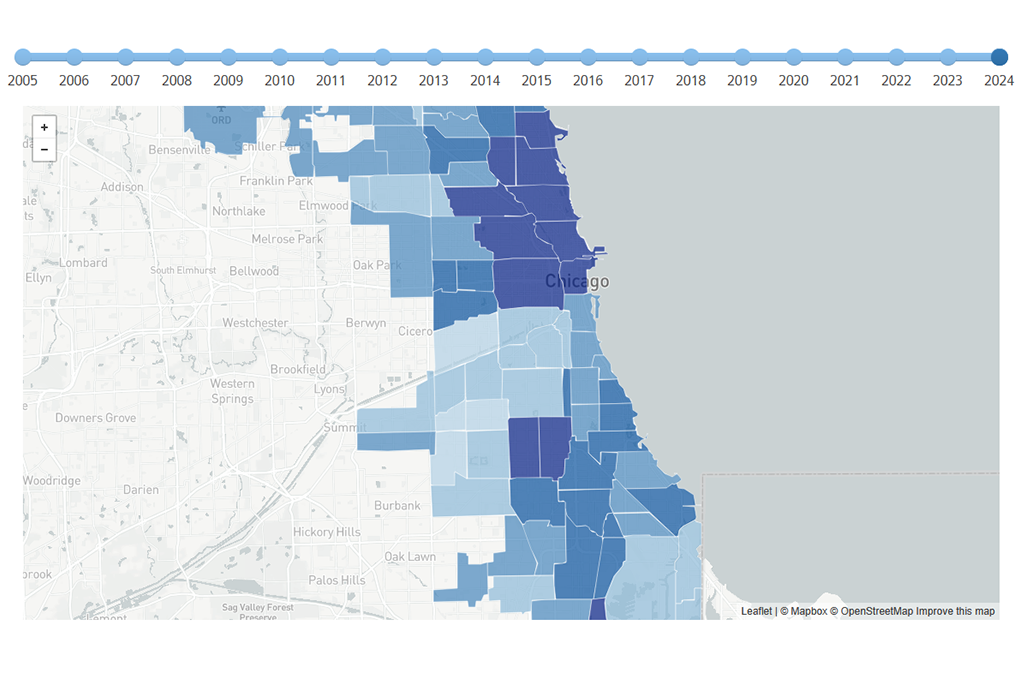

Data for 2012 show that cash purchases of distressed properties continue to present a distinct spatial pattern in Cook County that is concentrated in weaker housing markets where there continues to be a large supply of foreclosure-distressed properties. However, high levels of cash purchases of non-distressed properties occur throughout the County in both weak and strong housing markets.

The map below shows the share of single family and condominium home sales in 2012(1) that were purchased in cash and part of a non-distressed transaction. Census tracts in Cook County with the highest levels of this type of sale are shown in the darkest shades of brown. Census tracts with high levels of cash non-distressed purchases of single family homes and condominiums include tracts within Chicago neighborhoods in stronger markets in the Loop, Hyde Park, and the Near North Side. Weaker markets with high levels of non-distressed cash purchases include census tracts in Englewood, New City, and Greater Grand Crossing.

.jpg") Map showing share of sales in 2012 that were non-distressed residential properties purchased in cash in Cook County by census tract

Map showing share of sales in 2012 that were non-distressed residential properties purchased in cash in Cook County by census tract

A closer look at cash purchases of non-distressed properties

Though cash purchases of non-distressed properties occur throughout the County, a closer look at individual transactions in which non-foreclosure-distressed properties were bought with cash within a few of these markets shows distinct differences in the level of total sales activity, property type, price, and buyers in these neighborhoods. For example, in one census tract in the Loop in 2012, there were 146 total single family or condominium sales and 65.1 percent of those transactions were cash purchases of non-distressed properties. Of these, 75.8 percent were units purchased with cash in one single condominium building. The vast majority of these properties were purchased directly from the developer at a median price of approximately $200,000.

Non-distressed properties purchased in cash in one census tract in Chicago’s New City Community Area look very different. Total sales activity in this census tract in 2012 was extremely low with only 12 total purchases of which six were non-distressed properties purchased with cash. These properties ranged in price from $6,000 to $25,000 and were likely discounted by the broader foreclosure-distressed conditions present in the market regardless if the purchase itself was directly related to a foreclosure.

In Englewood, another historically foreclosure-distressed neighborhood, there were 47 total single family or condominium sales in one census tract, 87.2 percent of which were non-distressed properties purchased with cash. Of these, 90.2 percent were single family homes purchased by Norfolk Southern Railroad – ostensibly as part of its $285 million rail yard expansion project in that neighborhood.

(1) The data used in this analysis are limited to non-bulk purchases of single properties.