Background

As the national unemployment rate surged to a record high during the first few months of the COVID-19 pandemic, federal legislators passed bills that expanded an unprecedented level of aid to unemployed households and largely prevented an anticipated surge of economic hardship. Meanwhile, local and state policies were enacted across the country to stabilize households on the brink of eviction and foreclosure.

Today, most of the temporary policies and programs protecting vulnerable households have ended, yet not all households have economically recovered. Nationally and in Illinois, low-wage workers are experiencing the slowest economic recovery while middle- and high-wage workers have met or exceeded pre-pandemic employment levels. A survey conducted during the fall of 2021 shows that nearly 40 percent of U.S. households remain with serious financial problems, and roughly a third report being in a worse financial situation today compared to the beginning of 2020.

This blog is a part of our series examining the impact of the COVID-19 economy on Chicago households and communities. The first and second installment of this series summarizes changing local, state, and federal policy interventions that provided housing and financial stability during the pandemic. This third installment discusses data, research, and programs to guide equitable recovery efforts as COVID-19 protections and assistance enacted during the first two years of the pandemic end.

As COVID-era protections end, renters face fewer affordable options

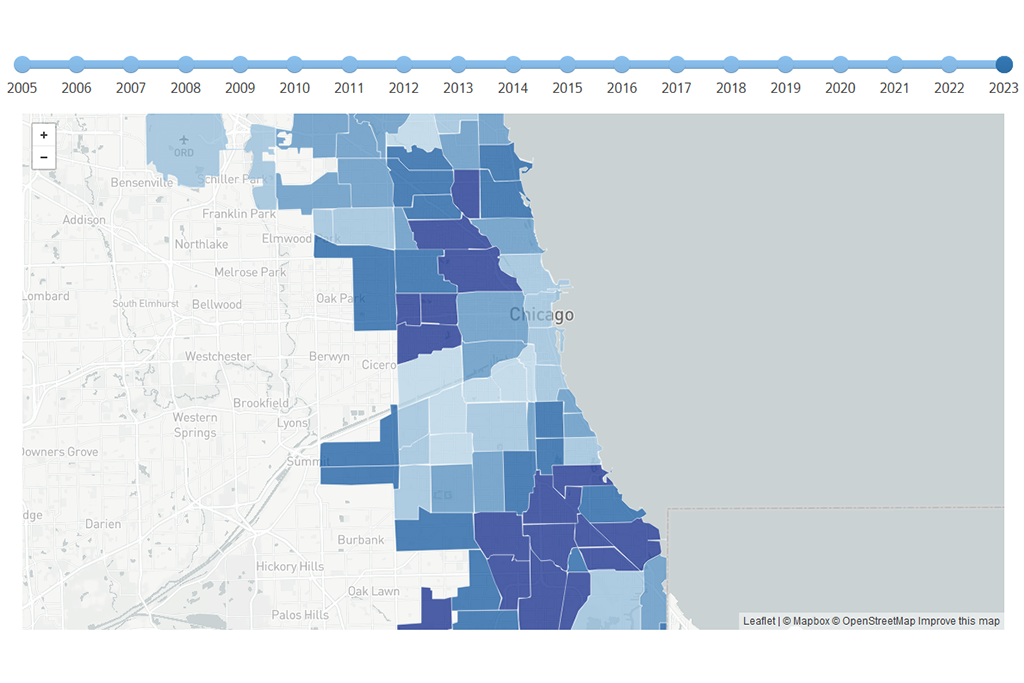

Preventing eviction and stabilizing vulnerable households is crucial as Cook County's rental housing market becomes increasingly out of reach to lower-income renters. IHS's 2021 State of Rental Housing report shows that since 2012, the share of very low-income renters earning below 30 percent of Cook County's median income continues to fall, while the supply of affordable rentals has seen long-term losses during the same period. From 2012 to 2019, the City of Chicago's affordable rental supply has declined by 9.5 percent, representing a loss of roughly 24,000 rental units. In some Chicago neighborhoods, as illustrated in the map below, the availability of affordable rental housing has declined at a much faster pace due to market pressures.

Figure 1. Percentage Point Change in the Share of Rental Units that are Affordable by Submarket in the City of Chicago, 2012-14 to 2017-19

Vulnerable renters and affordable housing advocates fear a growing number of evictions

A patchwork of local, state, and federal eviction moratoria served as a temporary solution to stabilize households that fell behind on rent payments. As rent arrears accumulated for unemployed and struggling renters, advocates hoped that the eviction moratoria would keep at-risk households in place while jurisdictions continued to distribute emergency rental assistance (ERA).

However, the Supreme Court struck down the second version of the CDC's eviction moratorium in September 2021, and Illinois' statewide eviction moratorium was phased out in early October. Meanwhile, expanded unemployment benefits ended in early September 2021. Following the end of these protections and assistance programs, vulnerable renters and affordable housing advocates feared that the Chicago region would see a spike in eviction. The latest Census Pulse Survey estimates that as of early February 2022, roughly 23 percent of Illinois renters were behind on their rent and approximately 55 percent of Illinois renters behind on their housing payments anticipate a very likely or somewhat likely chance of eviction within the next two months.1 Even as the economy continues to recover, renters that experienced unemployment during the pandemic may continue to face rent arrears today and likely require continued economic assistance. Of those that applied for the first and second rounds of emergency rental assistance in Cook County, roughly 55 percent of applicants were employed.

Gauging eviction risk using historical data

Where should city agencies and community-based organizations target eviction diversion and tenant stabilization strategies? To mitigate housing discrimination against Illinois renters experiencing housing instability due to the COVID-19 downturn, a statewide measure has sealed court records for eviction filings that occurred during the pandemic, limiting access to real-time data. To gauge potential eviction risk today, affordable housing policymakers and practitioners must primarily rely on data and trends on pre-pandemic housing and economic vulnerability.

Existing research shows that low-income households, women of color, and families with children disproportionately experienced eviction before the COVID-19 pandemic. In addition, IHS's preliminary analysis of potential neighborhood-level economic impacts from the pandemic shows that in Chicago, lower-income households, renter households, and Black and Latinx workers were more likely to work in occupations experiencing mass COVID-19 related layoffs.

Figure 2. Number of Working Renter Households in Vulnerable Occupations that are Cost-Burdened by Submarket in Chicago, 2018

Households that were already housing cost-burdened and experienced unemployment during the pandemic are likely at increased risk of eviction and housing instability, particularly if these households still have rent arrears and are navigating economic uncertainty due to COVID-19 variants, fewer to no childcare options, or lack of economic opportunity. IHS's analysis of pre-pandemic 2018 data shows that submarkets Bronzeville/Hyde Park, Humboldt Park/Garfield Park, and Uptown/Rogers Park had the most significant number of renter households that were likely already cost-burdened at the start of the pandemic and had a household member working in an occupation susceptible to mass layoffs due to early shelter-in place rules. On the city's south side, Englewood/Greater Grand Crossing and Auburn Gresham/Chatham had the highest concentration of cost-burdened renters working in vulnerable occupations (Figure X).

Data published by the City of Chicago's Department of Housing mirror these trends: Chicago's third round of the Emergency Rental Assistance Program (ERAP) received the most applications from ZIP codes within these larger submarkets on Chicago's South and West sides. Some of these communities also had high rates of pre-pandemic eviction filings and data from the Cook County Sheriff on executed evictions cases, a proxy for evictions filings while court cases remain sealed, show that the ZIP code that encompasses South Shore and parts of Woodlawn recorded the highest number of evictions in autumn, 2021.

Agencies continue to disburse emergency rental assistance

While the slow pace of many ERA programs across the country failed to keep up with growing need from renters, the Illinois Housing Development Authority's (IHDA) Emergency Rental Assistance Program became a model for an efficient and equitable ERA program, prioritizing lower-income households and communities in greatest need. IHDA grew internal capacity to handle a large volume of applications and developed strong partnerships with community-based organizations to conduct targeted outreach. In 2020, Illinois was the only state in the country to disburse its ERA funds fully and has become one of the largest providers of rental assistance, assisting nearly 110,000 households since the pandemic began.

However, emergency rental assistance programs in Illinois and across the country faced many challenges and were not immune to criticism. Despite recommendations to lessen application requirements in order to speed up ERA distribution, these requirements likely prevented vulnerable renter households from applying and accessing much-needed rental assistance. According to the National Equity Atlas, approximately half of Illinois renter households with arrears have not applied to any ERA program. Despite changes to policies that allow more flexibility, some households might have challenges accessing rental assistance, such as households that rely on informal housing arrangements and undocumented residents who may be less willing to pursue assistance programs due to uncertainty around the impact of immigration status on eligibility or language barriers.

The share of homeowners in forbearance reaches an all-time low

At one point during the pandemic, approximately 7.6 million borrowers were enrolled in a mortgage forbearance plan, totaling 15 percent of all mortgage borrowers. Forbearance plans allowed struggling homeowners to pause their monthly mortgage payments for an initial 12 months, which was subsequently extended to 18 months. As of December 2021, approximately 90 percent of borrowers have exited their forbearance plans, and roughly 75 percent of these exits resulted in a loan modification, extension, or another repayment plan. Additionally, the CARES Act's temporary foreclosure moratorium kept homeowners that were at risk of immediate foreclosure in their homes. These protections kept foreclosure filings low during 2020 (for an interactive map of foreclosure activity in 2020, click here).

Figure 3. Residential Foreclosure Filings per 100 Residential Parcels by City of Chicago Community Area, 2020

The foreclosure moratorium ended in June 2021, and the option for borrowers to opt into a forbearance plan ended in September 2021. To protect the influx of borrowers at risk of foreclosure as their forbearance plans end, the Consumer Finance Protection Bureau (CFPB) passed additional safeguards active from August to December 2021 that prohibited mortgage services from initiating a foreclosure and required servicers to inform borrowers of their options.

Avoiding similar outcomes from the last recession

Despite a record low share of mortgages in forbearance, borrowers that remain in forbearance today are likely more financially vulnerable than those who have exited forbearance with a repayment or loan modification plan. In December 2021, twice as many borrowers were more than 90 days late on their loans compared to pre-pandemic levels, totaling roughly 500,000 seriously delinquent borrowers. As of January 2022, the CFPB's rule ended and mortgage services are allowed to initiate foreclosure filings.

While the number of foreclosures resulting from the COVID-19 economic recession is expected to be far fewer than foreclosures seen during the Great Recession, housing advocates remain concerned about the racial, economic, and neighborhood-level impacts of foreclosures today. Throughout the pandemic, the share of Federal Housing Administration (FHA) insured mortgages in forbearance has remained elevated compared to other mortgage loans, and FHA borrowers were more likely to stay in forbearance plans for a longer period, signaling financial hardship. These FHA loans are held by a higher share of borrowers of color and lower-income borrowers, and they also comprise a higher share of mortgage loans in communities of color. Amid record-low foreclosure filings in 2020, the few filings that occurred were concentrated in Chicago's communities of color. Some of the same communities are still recovering from the impacts of the Great Recession.

Figure Y: Foreclosure Filings per 100 Residential Parcels by Chicago Community Area, 2020 Source: IHS Data Portal

Seriously delinquent homeowners exiting forbearance with few options other than to sell will be entering a housing market with strong house price growth and limited supply. IHS's House Price Index shows that during the pandemic, the largest year-over-year house price growth occurred in communities of color, potentially mitigating foreclosure risks. Nevertheless, not all borrowers who avoid foreclosure by selling their homes will be in a positive financial position. When factoring in 18 months of deferred payments, an estimated 23 percent of FHA and VA borrowers were in forbearance plans had less than 10 percent equity in their homes. If these households are unable to buy a home, they will likely need to find rental housing in an increasingly competitive market.

Vulnerable renters and homeowners need continued assistance

A study found that the expansion of federal assistance programs resulted in a 45 percent drop in the national poverty rate – from 13.9 percent in 2018 to 7.7 percent in 2021. As some of these programs were temporary stabilization measures that kept renters and homeowners from the brink of eviction and foreclosure and have now ended, struggling households may be at risk of continued housing insecurity and destabilization.

To help prevent vulnerable renters from falling through the cracks, a new court-based program developed between Chicago and Cook County agencies and a coalition of legal aid organizations seeks to connect renters to emergency rental assistance the first time they appear in court for an eviction filing. The goal of the program is to prevent a potential eviction by providing rental assistance to these households so that by their next court date, the eviction filing can be dismissed. During Cook County's second round of rental assistance funding, approximately 1 in 5 applicants that received rental assistance were facing eviction.

An additional $500 million in rental assistance was made available in the fall of 2021 for Illinois landlords and tenants. The Treasury Department is also capturing unspent emergency rental assistance dollars from jurisdictions that have spent a low share of their allocated ERA funds with plans to redistribute unspent ERA to high-performing programs and high need areas. While states and localities across the country were building ERA programs from scratch, the newly developed program infrastructure, internal systems, and increased capacity and expertise to distribute such large amounts of rental assistance will likely aid in ongoing recovery efforts.

Additional resources will also be available to homeowners. The Illinois Homeowner Assistance Fund will open in the spring of 2022 and provide a total of $387 million to struggling homeowners across Illinois. Recently, Illinois launched the Low-Income Household Water Assistance Program to assist lower-income homeowners with water debt.

All signs indicate that housing costs will continue to increase as the economy recovers

Rents and home prices increased substantially in 2021 and are expected to grow further in 2022. While many believe price growth will slow for single-family homes due to rising interest rates, most analysts anticipate the market will remain highly competitive as inventory stays low. Additionally, many of the key inputs affecting housing costs for existing landlords and homeowners such as property taxes and insurance are expected to grow. While lower-wage workers have experienced recent income growth, it remains unclear how sustained that growth will be and how that growth will compare with the rising cost of housing.

All of these signs highlight an ongoing need for policies to support lower-income renters, homeowners on fixed incomes, small-scale landlords, and others who may be vulnerable to housing instability and economic disruption. While the worst of the pandemic economy may have passed, a substantial amount of uncertainty and risk remains, which amplify the importance of data, research, and programs to inform and guide an equitable recovery.

1. Week 42 Household Pulse Survey: January 26, 2022 – February 7, 2022. Table 3b. Likelihood of Having to Leave this House in Next Two Months Due to Eviction, by Select Characteristics and Table 1b, Last Month’s Payment Status for Renter-Occupied Housing Units, by Select Characteristics