This update of the Institute for Housing Studies (IHS) Cook County House Price Index highlights changing prices for single family homes through the second quarter of 2015 in 16 City of Chicago submarkets and 17 submarkets primarily in suburban Cook County. A detailed discussion of the Index is below. To view a full page interactive graph with a map and data for all submarkets go here. Underlying price index data can be found here.

Key Findings

Year-over-year price changes

- Areas with large increases in prices since last year include Chicago submarkets Humboldt Park/Garfield Park and Austin/Belmont Cragin, where price levels increased nearly 20 percent and over 15 percent, respectively. Figure 1 highlights the countywide variation in year-over-year price trends. Many of the areas experiencing the largest price increases over the past year are those distressed areas on the south and west sides of the city that started their recovery more recently.

- Areas with flat or declining year over year price trends are suburban Calumet City/Harvey and Chicago Heights/Park Forest where prices declined 0.7 percent year over year and increased just 0.4 percent, respectively.

Figure 1 Year over Year Change, Q2 2015 Cook County Submarkets

Figure 1 Year over Year Change, Q2 2015 Cook County Submarkets

Recovery from bottom

- As of the second quarter 2015, many markets in Cook County continue to see double digit price recovery from their lowest levels post-recession. Areas with the largest increases from price bottoms include Logan Square/Avondale and struggling but strongly rebounding Humboldt Park/Garfield Park. These areas both have price levels as of the second quarter 2015 that are more than 50 percent higher than their respective price bottoms.

Peak to current

- As of the second quarter 2015, prices in the Lake View/Lincoln Park and Lincoln Square/North Center submarkets in the City of Chicago were nearly at peak levels. At this time, price levels in these submarkets were just 0.1 and 0.2 percent below prices last seen at their respective heights in the first quarter of 2015 and the third quarter of 2007.

- Areas that have shown slight improvement since the fourth quarter of 2014 but continue to be well below peak levels include the area in and around Englewood/Greater Grand Crossing and Humboldt Park/Garfield Park in the City of Chicago. In both of these areas, prices remain over 56 percent off peak levels seen during the housing bubble.

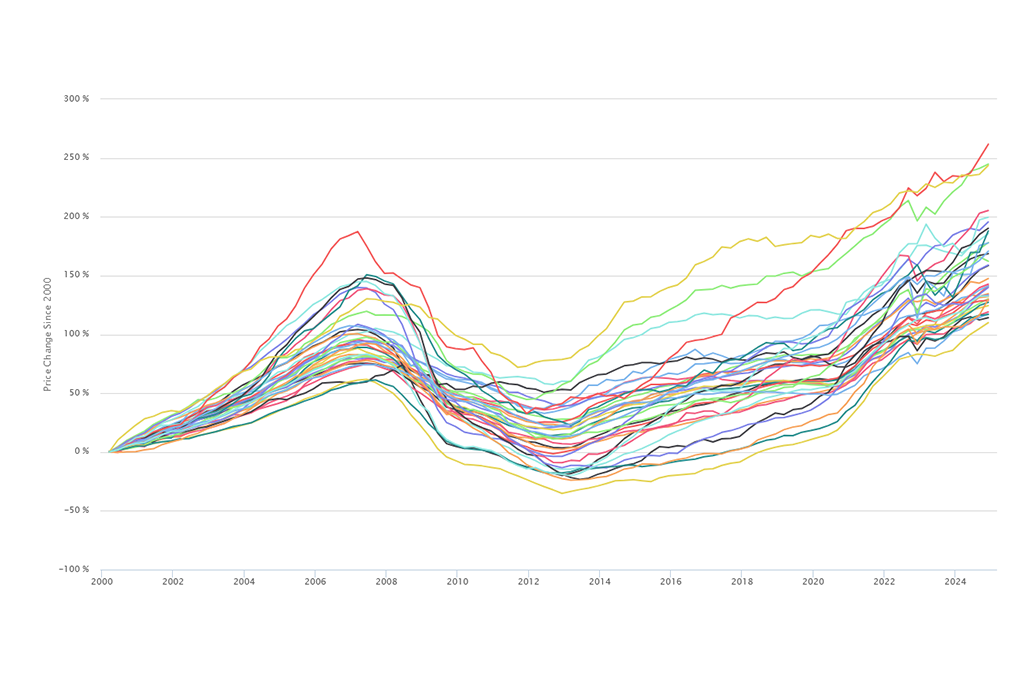

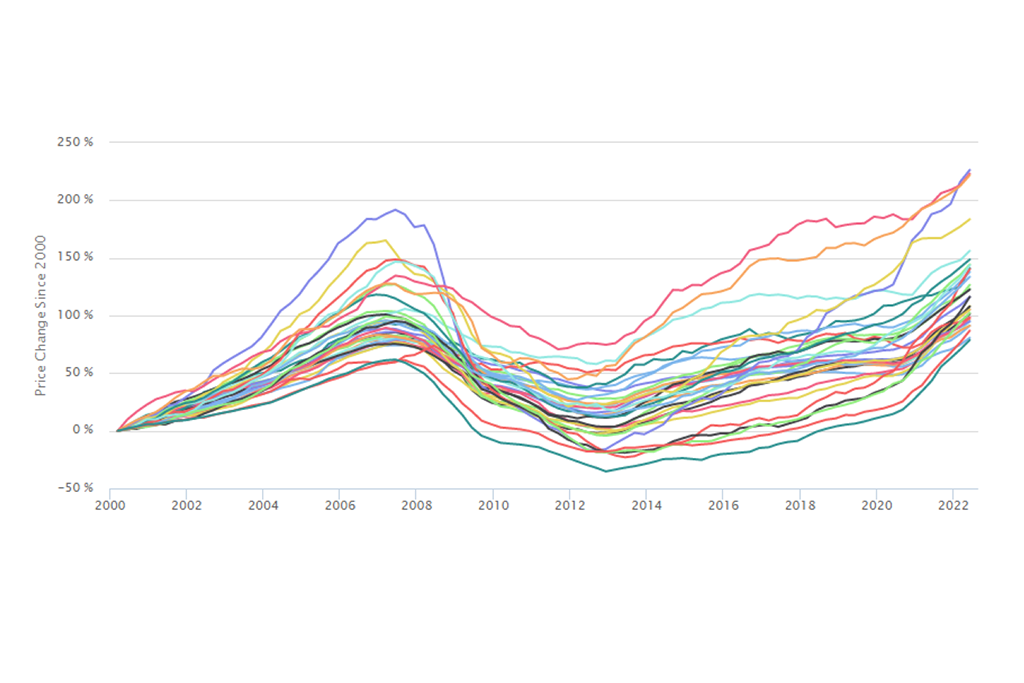

Price changes since 2000

- As of the second quarter 2015, three Cook County submarkets continue to experience price levels below what they were in the year 2000. These include suburban Cook County submarkets Calumet City/Harvey and Chicago Heights/Park Forest, and City of Chicago submarket South Chicago/West Pullman. Prices in suburban Calumet City/Harvey were 23.7 percent less than levels in the year 2000, while price levels in the area in and around suburban Chicago Heights/Park Forest were 11.7 percent below prices in 2000. In the City, only the South Chicago/West Pullman submarket is still experiencing price levels lower than year 2000 prices.

- Conversely, price levels in three Chicago submarkets were more than double what they were in 2000. This includes the Logan Square/Avondale and West Town/Near West Side submarkets (both at 126.9 percent above 2000 levels) and the area in and around Lincoln Square/North Center, where prices increased over 109 percent from 2000 levels as of the second quarter of 2015.

To view a full page interactive graph with a map and data for all submarkets go here. Underlying price index data can be found here.

Background on Price Indices

House price trends are one of the most important indicators of a neighborhood’s economic health, and understanding how these trends vary within the City of Chicago and suburban Cook County is critical to those working to develop policies and investment strategies sensitive and responsive to local market dynamics and household financial conditions. To help housing stakeholders, policymakers, and the public understand this issue better, the Institute for Housing Studies (IHS) has developed a submarket-level Cook County house price index to track quarterly price trends for single family homes in 16 submarkets in the City of Chicago and 17 submarkets in suburban Cook County.

In recent years, substantial focus has been paid to the importance of house price trends as a national or regional indicator of economic conditions, but growing attention is being paid to the implications uneven price declines and recoveries across neighborhoods have for communities and their residents. Neighborhoods with rapidly rising prices may be those facing current or future housing affordability concerns, while areas with slow price recovery may need strategic investment to rebuild demand for housing. Additionally, the uneven nature of house price declines and recovery across neighborhoods is a stark illustration of the growing divide between thriving and struggling communities and households. Home equity is one of the key vehicles for families to build wealth, and the variation in price trends can be an indicator of household financial conditions across communities measured by the level of home equity gained and lost by households and neighborhoods over time.

More About IHS' Cook County Submarket Indices

The submarkets in IHS’s price index are based on Public Use Microdata Areas (PUMAs) from the 2010 US Census. There are 16 submarkets in the City of Chicago and 17 that are primarily in suburban Cook County. In the City of Chicago, the submarket surrounding the Loop has been excluded because of insufficient levels of single family home sales. Click here for a reference guide to the community areas and suburban municipalities found in each submarket. Additional detail about the model can be found at the end of this analysis.

The discussion below highlights four key metrics for analyzing house price trends and describes their patterns and their implications for communities:

Year over Year – This metric illustrates the short-term price trend and compares the current price level as of the second quarter 2015 with the price level in the second quarter 2014. Areas with large changes in price levels tend to be a mix of markets with recent increased demand. These include highly foreclosure distressed areas where prices are starting to recover, and rapidly appreciating “hot” markets. Historically strong markets tend to have low but steady appreciation year over year. Interpreted in conjunction with other price trend indicators, year over year price changes can be helpful in identifying rebounding markets with stabilizing prices.

Recovery from Bottom – This metric measures the change in price level from a submarket’s lowest point after the 2008 collapse of the housing market to the second quarter of 2015. It tracks the speed of recovery of single family house prices from the point that prices in that submarket reached their recent lowest price level. This indicator is an important measure for recent buyers who purchased properties near the bottom of the market and who are trying to understand the return on that investment. It is also a valuable indicator for understanding where investment has been flowing in recent years. This “recovery” metric is a product of recent demand for housing outstripping the supply of homes for sale in these areas. This demand could be driven by owner occupants competing for a limited supply of for-sale housing in “hot” markets or investors competing for the dwindling supply of low cost properties in more distressed markets. This recovery metric should be interpreted in conjunction with other price trend data points, however.

Peak to Current –This metric measures the difference between a submarket’s peak price level at the height of the housing boom and the current price level as of the second quarter of 2015, and it captures the recovery of a neighborhood’s house prices towards previous price peak levels. Often, neighborhoods that saw substantial build up in prices during the housing bubble, experienced equally dramatic declines. While, those price peaks were often inflated and unsustainable, recovery towards those peaks is an important benchmark for homeowners who bought their homes or obtained a mortgage from 2005 to 2007 when prices were at their highest.

Many homeowners are reluctant to sell their homes for less than what they paid, and, in cases where a mortgage is involved, areas that are well below previous peak values are likely to have larger numbers of underwater or near underwater homeowners. As values get closer to previous peak levels, more homeowners are likely willing and able to sell, more households will exit underwater status, and equity lost during the housing crisis is rebuilt. In areas where values remain well below peak levels, many homeowners likely remain underwater. Owning more on a mortgage than what a property is worth limits an owner’s ability to sell their property and puts a greater strain on a household’s financial conditions.

Price trends since 2000 – This metric tracks the change in price levels from the first quarter of 2000 to the second quarter 2015 and measures long term price trends. The variation in neighborhood price trends since 2000 is a key indicator of the impact the housing crisis and uneven housing recovery has had not just on local housing markets, but also on long term homeowners. Home equity is a key asset for both lower- and higher-income households, and increasing equity over time is one of the ways that both lower- and higher-income households build wealth. Areas where there has been limited long term price appreciation are areas where long time owners benefit less from increasing home equity compared with long term owners in areas with significant appreciation.

The Model

Using its data clearinghouse, IHS has developed a hedonic price index model to provide a stable mechanism to track submarket-level price trends. Unlike a repeat sales model which requires a matched pair of sales on a single property and can be less stable at smaller geographies, a hedonic model combines data on a property’s sales price with data on the physical characteristics of that property and its location relative to key amenities or disamenities. The statistical model controls for factors that contribute to price and allows for the development of an index tracking price changes of the typical, non-distressed home over time and is ideal for tracking price trends at the submarket level. Click here for more information on IHS’s hedonic price index model.