Photo: Evelyn Ryan

This analysis builds on recent IHS research documenting the challenges and opportunities for expanding homeownership access and wealth building for Black and Latino households by highlighting the important role that 2 to 4 unit buildings play in homebuying for Chicago’s borrowers and neighborhoods of color. The analysis helps make the connection between policy priorities around preserving 2 to 4s with those that advance homeownership and wealth-building for moderate- and middle-income Black and Latino households.

Background

More than any other type of housing stock, 2 to 4 unit buildings serve a dual purpose of providing homes for both owner-occupants and renters, and they are the cornerstone of Chicago’s unsubsidized lower-cost rental housing stock. In Chicago’s majority Hispanic or Latino and predominately Black communities, 2 to 4 unit buildings represent a significant share of the overall housing stock, and comprise the vast majority of housing units in neighborhoods like Little Village, Brighton Park, New City, and West Garfield Park. For Black and Hispanic renter and owner households, 2 to 4’s are often home. Over 73 percent of rental units in 2 to 4 flats are occupied by a person of color, and the majority of 2 to 4’s are owned by a Black or Latino head of household.1 Examining data of homeowner exemptions by the underlying race and ethnic composition of neighborhoods, IHS research has found that roughly 62 percent of 2 to 4 unit buildings in majority Hispanic or Latino neighborhoods and roughly 43 percent of 2 to 4s in predominately Black neighborhoods have a homeowner’s exemption.

Despite its importance to many Chicago neighborhoods, the 2 to 4 unit stock has also been uniquely threatened in recent years. During the Great Recession and foreclosure crisis, nearly 30 percent of the 2 to 4 unit stock was hit by a foreclosure filing, more than any other type of property in Chicago, and levels of foreclosure distress were far higher for 2 to 4 unit buildings in Chicago’s predominantly Black communities. More recently, the 2 to 4 unit stock has been under pressure from market forces tied to gentrification and disinvestment. Citywide, more than 4,800 2 to 4 unit properties representing nearly 11,800 rental and owner-occupied units were lost between 2013 and 2019 – primarily replaced by single-family homes in expensive neighborhoods but also lost to demolition and deterioration in more distressed markets.

Given the importance of 2 to 4 unit buildings in Chicago, preservation of the stock has been a growing policy priority in recent years. Strategies have focused on the unique roles that 2 to 4 unit buildings play in providing homeownership opportunities, multigenerational living opportunities for families, and income-generating opportunities for landlords. Some efforts target 2 to 4 flat building investors and are oriented around preserving rental units in 2 to 4s as “naturally occurring” affordable rental housing, while other strategies seek to stabilize existing owner-occupants of 2 to 4s. Further strategies are focused on encouraging new investment in the 2 to 4 unit stock as a means to support building household and community wealth – particularly for Black and Hispanic or Latino households and neighborhoods.

Recent research has highlighted both progress and ongoing challenges associated with increasing the number of homeowners of color. Nationally, the homeownership rates for Black and Latino households grew steadily in recent years, particularly during the first years of the COVID-19 pandemic. However, despite this growth, homeownership levels for Black and Latino households still lag behind those of white households. Recent IHS research highlighted strong growth in home purchase lending for Black and Latino households in Chicago since 2012. Other research shows growth in Black and Latino homebuying during the pandemic, though substantial gaps remain.

This analysis examines recent homebuying activity in Chicago to explore the role that 2 to 4 unit properties play for Black and Hispanic or Latino households and neighborhoods citywide. It uses data collected through the Home Mortgage Disclosure Act (HMDA) to analyze patterns in owner-occupied home purchase lending on 2 to 4 unit buildings in Chicago between 2018 and 2021.2 It shows that Black and Latino borrowers are more likely to purchase 2 to 4’s than white borrowers and while lending on 2 to 4’s represent a fraction of overall home purchase loans citywide, mortgage loans on 2 to 4 unit properties are a critical portion of the lending environment for borrowers of color and in communities of color. Further, analysis by borrower income shows that 2 to 4 homebuyers are very often moderate- or middle-income, driven by the substantial share of moderate- and middle-income Black and Latino households that purchase 2 to 4s.3 These findings further demonstrate the importance of 2 to 4s as a housing type in Chicago and as a pathway for homeownership and potential wealth building for moderate- and middle-income Black and Latino households.

Key Findings

Citywide, the vast majority of owner-occupied home purchase loans are for single-family homes or condominiums. Between 2018 and 2021, there were roughly 100,000 mortgages on 1 to 4 unit properties in Chicago with over 88,000 of those loans for single-unit properties, either single-family homes or condominiums. Over the same period, roughly 8,500 loans were originated on owner-occupied 2 unit properties, and roughly 3,000 on owner-occupied 3 and 4 unit properties. While overall levels of lending increased annually between 2018 and 2021, the share of total loans for 2 to 4 unit properties remained flat during this period. Annually between 2018 and 2021, roughly between 11 and 12 percent of all 1 to 4 loans originated in Chicago were to borrowers purchasing 2 to 4 unit buildings.

Figure 1. Number of Owner-Occupied Home Purchase Loans by Property Type, 2018 to 2021

Figure 2. Owner-Occupied Home Purchase Loans to 1-Unit and 2 to 4 Unit Properties in Chicago, 2018 to 2021

Black and Latino homebuyers are much more likely to purchase a 2 to 4 property than other borrowers. Between 2018 and 2021, 11.5 percent of all owner-occupied loans for buildings with four or fewer units citywide were to owners purchasing 2 to 4 unit properties. This share was substantially higher for Black and Latino borrowers. During this same time period, over 24 percent of Black homebuyers and nearly 20 percent of Latino homebuyers purchased a 2 to 4 flat. Conversely, less than six percent of white homebuyers in Chicago purchased a 2 to 4 unit property during this period – fewer than 3,000 of roughly 45,000 loans to white borrowers were for 2 to 4s.

Figure 3. Share of Owner-Occupied 1 to 4 Unit Home Purchase Loans that are to 1 to 4 Unit Properties by Borrower Race and Ethnicity, 2018 to 2021

Black and Latino homebuyers play a large role in the 2 to 4 unit lending market. Figure 4 examines the composition of homebuyers of single-family homes and condominiums and 2 to 4 flats by the race/ethnicity of the borrower. It shows that Black and Latino homebuyers accounted for 11.5 and 16.9 percent of owner-occupied home purchase loans on single-family homes and condominiums between 2018 and 2021, respectively. Over the same period, Black homebuyers accounted for over 28 percent of owner-occupied loans on 2 to 4 unit properties while Latino borrowers accounted for over 32 percent of loans on 2 to 4s. Comparatively, white borrowers accounted for roughly 51 percent of loans for single-family homes or condominiums and 24 percent of loans for 2 to 4 flats.

Figure 4. Distribution of Owner-Occupied Loans to Single Family/Condominiums and 2 to 4 Unit Properties by Borrower Race and Ethnicity in Chicago, 2018 to 2021

Most 2 to 4 unit homebuyers are moderate- or middle-income. Figure 5 compares the distribution of home purchase loans for single-unit and 2 to 4 unit properties by borrower income, and Figure 6 breaks out all 2 to 4 borrowers by the race, ethnicity, and income of the homebuyer. Figure 5 shows that while upper-income homebuyers purchased roughly 50 percent of loans for single-family homes and condominiums, they only purchased roughly 32 percent of loans for 2 to 4’s. A much larger proportion of borrowers for 2 to 4s were moderate- and middle-income compared to those of single-unit properties – just 18.3 and 24.8 percent of single-unit homes were purchased by a moderate- or middle-income homebuyer compared to 27.6 and 33.6 percent of all 2 to 4s, respectively. Examining the income characteristics of 2 to 4 borrowers by race and ethnicity, Figure 6 illustrates that over 73 percent of Black and Latino homebuyers of 2 to 4 flats were moderate- or middle-income compared to just 36.3 percent of all white 2 to 4 homebuyers. In 2021, the median income of a Black or Latino homebuyer of a 2 to 4 unit property purchased with a mortgage was $75,000 and $72,000, respectively. By comparison, the median income of a white or Asian 2 to 4 homebuyer in 2021 was $123,000 or $100,000, respectively.

Figure 5. Distribution of Owner-Occupied Loans for Single Family/Condominiums and 2 to 4 Unit Properties by Borrower Income Level in Chicago, 2018 to 2021

Figure 6. Composition of Owner-Occupied Loans to Moderate- and Middle-Income Homebuyers of 2 to 4 unit Properties by Borrower Race and Ethnicity in Chicago, 2018 to 2021

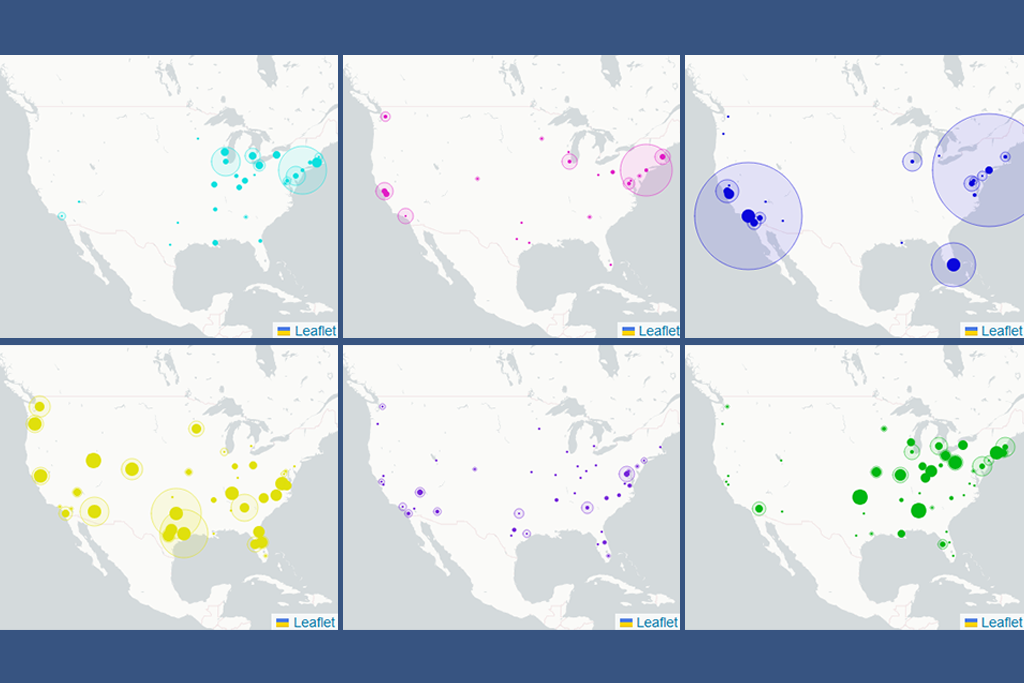

Geographically, 2 to 4 homebuying by borrower race and ethnicity follow well-known patterns of residential segregation in Chicago and the general built environment but also shows patterns of diversity in 2 to 4 homebuying in pockets of the city. The interactive map below highlights overall patterns of the approximate location of owner-occupied home purchase lending on 2 to 4 unit properties citywide. In the map, each dot represents an owner-occupied home purchase loan originated between 2018 and 2021, randomly generated within a census tract. Dots are color-coded to represent the race and ethnicity of the homebuyer. To explore these patterns further, click within a Chicago community area to generate a pop-up window with summary data on the number of owner-occupied 2 to 4 home purchase loans between 2018 and 2021 and the distribution of those loans by the race and ethnicity of the borrower. Community area-level summary data are included in the report appendix. View a full-size version of the map here.

Figure 7. Randomized Dot Density of Owner-Occupied Home Purchase Loans on 2 to 4 unit Properties in the City of Chicago, 2018 to 2021

2 to 4 home purchase lending is concentrated on the South and West Sides of Chicago. The figure below highlights the density of owner-occupied 2 to 4 unit home purchase lending per 100 2 to 4 unit parcels and illustrates what neighborhoods have the highest density of 2 to 4 homebuying relative to its 2 to 4 unit housing stock since 2018. It shows South Side neighborhoods such as South Shore, Woodlawn, Auburn Gresham, Grand Boulevard, and Chatham had the highest concentration of owner-occupied home purchase loans on 2 to 4 unit properties when compared to their overall stock of 2 to 4’s in the housing market. For example, South Shore had 302 loans originated on 2 to 4 unit properties between 2018 and 2021 – 16 loans for every 100 2 to 4s or 16 percent of the 2 to 4 stock had a home purchase loan during this period.

Figure 8. City of Chicago Community Areas with the 15 Highest Densities of Owner-Occupied Lending on 2 to 4 Unit Properties, 2018 to 2021

Neighborhoods on Chicago’s South and West Sides also showed strong levels of investment from 2 to 4 owner occupants when compared to the broader distribution of the 2 to 4 housing stock. The chart below compares the distribution of Chicago’s 2 to 4 unit housing stock to the distribution of 2 to 4 unit owner-occupied home purchase loans. The chart illustrates where there were higher levels of recent investment in owner-occupied home purchase lending activity on 2 to 4s than would be expected based on the existing housing stock. For example, just under 6 percent of Chicago’s 2 to 4 flats are located in Austin, but 7.1 percent of all Chicago’s owner-occupied loans on 2 to 4s originated between 2018 and 2021 were originated in the Austin neighborhood – indicating strong demand for owner-occupied 2 to 4 homebuying in the community. Community area-level summary data are included in the report appendix.

Figure 9. Top 10 City of Chicago Community Areas with the Largest Gap in Citywide Share of Total 2 to 4 Parcels and Citywide Share of Total Owner-Occupied Loans on 2 to 4 Unit Properties, 2018 to 2021

Discussion

This report analyzed data on owner-occupied home purchase loans in the City of Chicago to characterize the homebuying market for 2 to 4 unit properties. The analysis added additional evidence to recent IHS research that documented the critical role that 2 to 4 unit buildings play for renters, owners, and neighborhoods of color. By documenting the central role that 2 to 4s play in Black and Hispanic or Latino homebuying, particularly for moderate- and middle-income homebuyers, this analysis helps connect policy priorities for preserving the 2 to 4 housing stock with those for increasing homeownership and wealth-building opportunities to Black and Latino borrowers.

To further leverage 2 to 4 unit buildings as a pathway to sustainable homeownership for households of color, it will be important not only to build on traditional supports for new homeowners such as down payment assistance programs and home buyer education but also to consider program features that accommodate the unique characteristics of the 2 to 4 unit stock such as landlord training. Additionally, given growing affordability challenges and the limited supply of move-in-ready housing, programs supporting the rehab or new construction of modestly-priced 2 to 4 unit properties for purchase will be important to facilitate the ability of moderate- and middle-income households to become homeowners, invest in their communities, and revitalize this critical component of Chicago’s housing stock.

IHS's work on this topic is generously funded by the Chicago Community Trust, the John D. and Catherine T. MacArthur Foundation, and the Polk Bros Foundation. IHS would like to thank the many individuals and organizations who shared their issue area expertise throughout the development of this report.

1. These data come from the American Community Survey and it is not possible to disaggregate owner-occupied 2 to 4 unit rental buildings from owner-occupied 2 to 4 unit condominium buildings. Therefore, a small percentage of units may be condominium units in 2 to 4 unit buildings. According to the source data, 55.8 percent of owner-occupied units in 2 to 4 unit buildings are owned by a Black or Hispanic/Latino head of householder.

2. All data referenced in the Key Findings section of this analysis are sourced from the Home Mortgage Disclosure Act (HMDA) and include all first-lien, owner-occupied, home purchase loans originated in Chicago from 2018 to 2021. Only records where race, ethnicity, income, and geography were populated were included in the analysis. Since 2018, regulators began to require that lenders report the number of units in a structure. Data pre-2018 do not have this feature and therefore analyses of longer-term patterns are not possible. Data on market context are from calculations of Cook County Assessor Data housed in the IHS Data Clearinghouse.

3. Low-income refers to borrowers with incomes below 50 percent of the area median income, moderate-income borrowers have incomes between 50 and 80 percent of the area median income, middle-income borrowers have incomes between 80 and 120 percent of the area median income, and upper-income borrowers have incomes at or above 120 percent of the area median income. Area median income is calculated annually by the Federal Financial Institutions Examination Council (FFIEC) and included in data from the Home Mortgage Disclosure Act (HMDA). In 2021, the FFIEC Chicago MSA median income reported was $87,100.